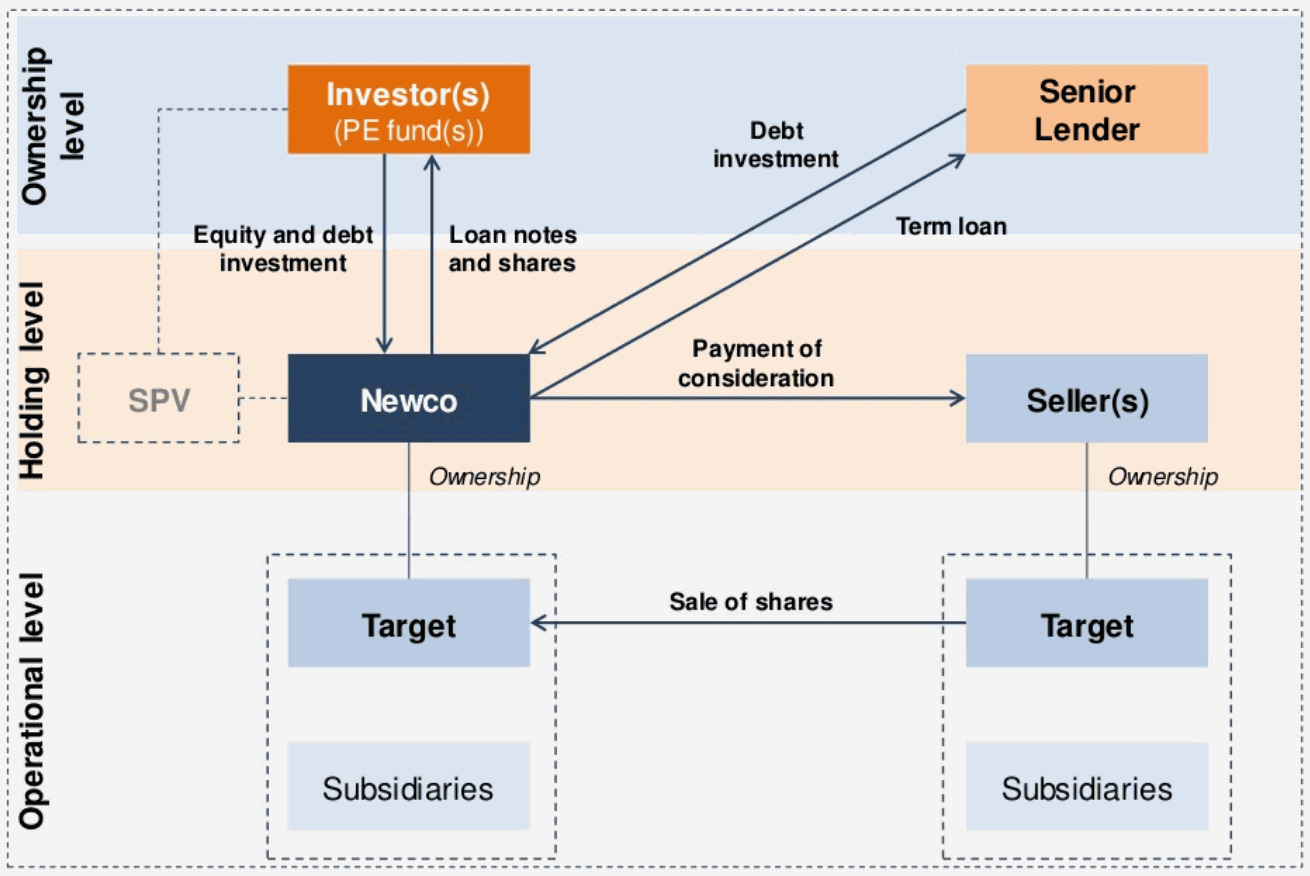

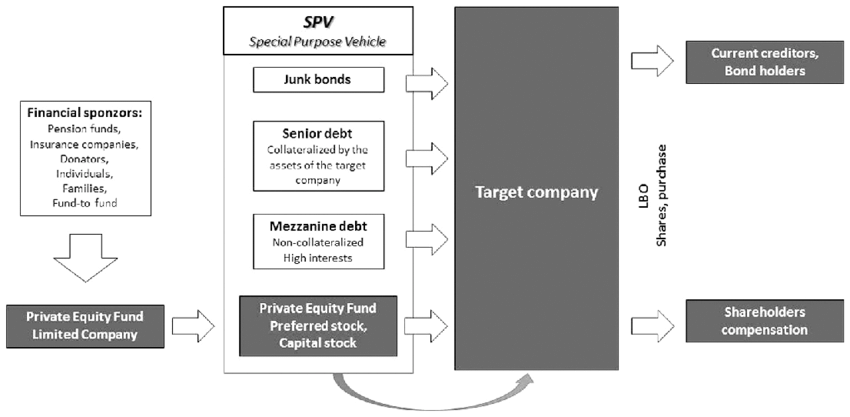

Leveraged Buy-Outs (LBOs)

Sponsor-led acquisitions financed via senior and mezzanine debt.

A leveraged buy-out (LBO) is the acquisition of a company using a significant amount of borrowed money, with the target's cash flows and assets supporting the debt. Matchpoint structures LBOs and arranges the senior and mezzanine financing.

As part of our M&A practice, Matchpoint Partners has originated and led $2+ billion of transactions across four continents, and every M&A mandate is led by a partner, from first call to close.

A leveraged buy-out (LBO) is the acquisition of a company using a significant amount of borrowed money, repaid from the target's cash flows, with the assets supporting the debt. Sized correctly, leverage amplifies equity returns; sized wrongly, it adds fragility. Matchpoint Partners structures LBOs and arranges the senior and mezzanine financing, modelling debt to a sustainable level for the specific target.

Our role on leveraged buy-outs (lbos) mandates

- Senior and mezzanine acquisition debt

- Sponsor-led transaction structuring

- Cash-flow-based debt sizing

- Returns and capital-structure modelling

Select transactions

Representative M&A mandates led by Matchpoint partners.

Sell-side M&A of a distressed US trophy landmark hotel.

M&A and growth for a core-banking services firm.

Chinese-controlled Italian gelato brand JV / cross-border merger.

M&A and equity raise for a gold & precious-metals mining firm.

Buy-side M&A of a UAE AI product firm by a Saudi IT-services group; synergy and dyssynergy quantification, consolidated due diligence.

Our proprietary research

Original, data-driven research from our team, relevant to this area.

Leveraged Buy-Outs (LBOs) — frequently asked questions

An acquisition funded largely by debt, repaid from the acquired company's cash flows, amplifying equity returns.

It depends on cash-flow stability and sector; we size debt to a sustainable level for the specific target.

A company suits a leveraged buy-out when it generates stable, predictable cash flows that can reliably service debt — typically with recurring revenue, defensible margins, modest capital expenditure and low cyclicality. Asset backing helps the security package, but cash-flow quality determines how much leverage the structure can sustain.

The main LBO risks are a downturn in cash flows that strains debt service, covenant breaches that hand leverage to lenders, refinancing risk when facilities mature and underinvestment in the business to prioritise repayments. Conservative debt sizing and genuine operational headroom are the principal protections.

An LBO structure typically layers senior debt at the base, mezzanine or subordinated debt above it, and sponsor and management equity at the top. Each layer carries different cost, security and rights; the mix is sized against the target’s cash flows to balance returns against resilience.

M&A advisers cover the full transaction: strategy and target screening, valuation, running the sell-side or buy-side process, due-diligence coordination, deal structuring and negotiation, and financing the acquisition. Post-merger-integration (PMI) consultants take over after close — 100-day integration planning, synergy capture and tracking, operating-model and systems integration, and talent retention. Matchpoint provides both ends: origination-to-close M&A advisory and the PMI planning that protects the value you paid for.

M&A advisory is senior-led guidance and execution across a merger, acquisition or divestment — from strategy, valuation and target or buyer identification through diligence, structuring, negotiation and completion. Matchpoint runs full sell-side and buy-side mandates, confidentially and partner-led from origination to close.

Yes — Matchpoint is UAE-licensed with partners in Dubai and Abu Dhabi, advising GCC business owners, corporates and investors on sell-side, buy-side and merger mandates, with cross-border reach into KSA, India, the UK and the US.

Matchpoint runs full sell-side mandates: we value the business, build the information memorandum, identify and approach buyers, manage diligence and negotiate to close — confidentially and senior-led throughout.

An MBO is led by existing management, an MBI by an incoming external team, and an LBO uses significant debt to fund the acquisition. We structure all three and arrange the acquisition finance.

We bridge a target's stand-alone enterprise value to the consideration paid, isolating hard, soft and financial synergies net of costs — so clients see exactly where value is created.

Matchpoint works primarily on a success fee, with a modest retainer to cover execution. Fees are agreed in writing up front and scaled to the size and complexity of the transaction — with no hidden costs.

Most sell-side and buy-side M&A processes run 4–9 months from mandate to completion, depending on diligence, regulatory approvals and negotiation.

A short, confidential scoping call and NDA; we structure the requirement and prepare materials, then run a competitive process across our 5,000+ investor and lender relationships, and negotiate to close — with a partner leading at every step.

Matchpoint Partners is based in the UAE and runs cross-border mandates across the UAE, KSA, India and the UK, with active deal activity in wider Europe, Singapore and the United States.

Matchpoint has originated and led $2+ billion of transactions, with equity tickets typically USD 5m–300m, debt USD 10m–500m+, real estate finance USD 20m–500m+, and fund placements for funds of USD 50m–1bn+.

Use the enquiry form, email ck.adya@matchpoint-partners.com, or call/WhatsApp +971 52 345 1119. Every mandate is led by a partner from the very first conversation.

Yes. Matchpoint runs discreet, confidential processes and discloses client identities only under a signed non-disclosure agreement (NDA).

More in M&A

Interested in leveraged buy-outs (lbos)?

Tell us your requirement and a partner will respond personally.