Building a Private Credit Allocation: A Family Office Framework for Risk, Yield and Liquidity

A family-office framework for building a private-credit allocation balancing risk, yield and liquidity.

Private credit has become a core allocation for sophisticated family offices, but building the allocation well requires more than chasing headline yield. This paper offers a framework for sizing the allocation, balancing risk, yield and liquidity, choosing between strategies and access routes, and avoiding the concentration and duration traps that catch first-time allocators.

A family-office framework for building a private-credit allocation balancing risk, yield and liquidity.

Part of Matchpoint Partners' proprietary research programme — original, data-driven analysis grounded in live deal experience. Read the full paper: framework, structures, worked examples and data.

Read the full research paper Explore our Alternatives practice

What this paper examines

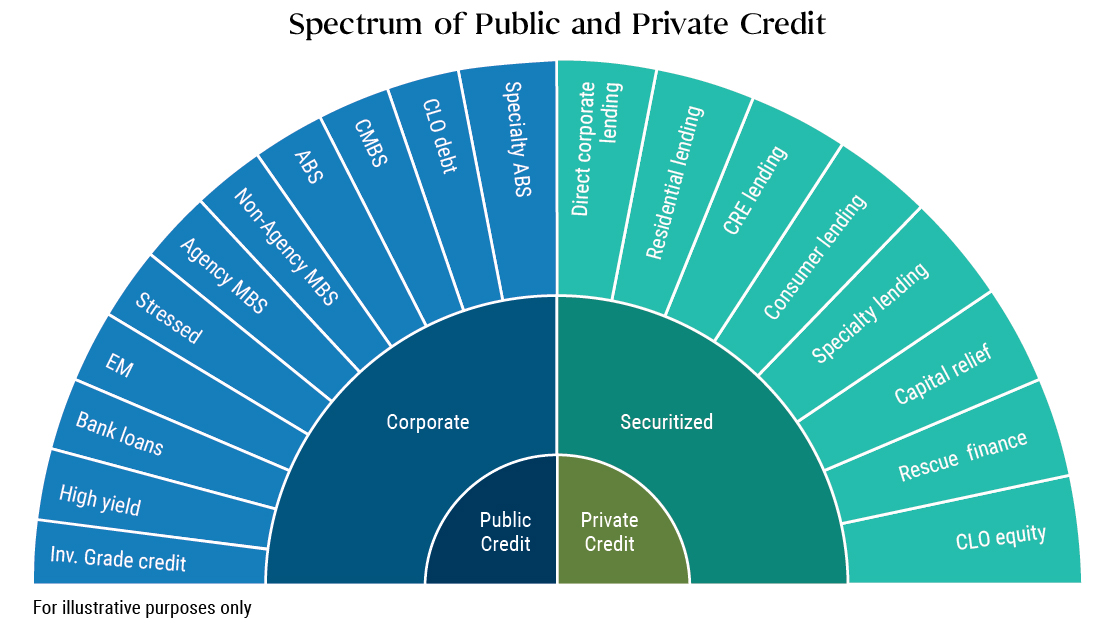

The paper provides a structured framework for a family office building a private-credit allocation from first principles. It begins with the role the allocation is meant to play — income, diversification, equity-risk reduction or opportunistic return — because that purpose drives every subsequent choice. It then maps the strategy spectrum, from senior direct lending through mezzanine and special situations to asset-backed and speciality finance, and explains how risk, yield and liquidity trade off along that spectrum.

Access routes receive equal attention: commingled funds, separately managed accounts, co-investments and direct lending each demand different levels of internal capability and offer different control, fee and liquidity profiles. The paper closes with portfolio-construction guidance — diversification across managers, vintages, sectors and geographies — and the warning signs that an allocation is drifting from its mandate.

Why it matters now

Private credit’s growth has brought a flood of new product of widely varying quality, and yields that look similar on paper can conceal very different risk. Family offices — including many in the GCC making their first dedicated allocation — are being marketed to aggressively. A disciplined framework for evaluating strategy, manager and structure is the difference between a durable income engine and an illiquid disappointment.

Key questions it answers

- How should a family office decide what role private credit plays in the overall portfolio — and how large the allocation should be?

- How do senior lending, mezzanine, special situations and asset-backed strategies differ in risk, yield and liquidity terms?

- When do funds, managed accounts, co-investments or direct lending make sense as access routes?

- What diversification and pacing rules keep a private-credit book resilient through a credit cycle?

Who should read it

Family-office principals and CIOs designing or expanding a private-credit allocation; investment-committee members who must approve and oversee it; and wealth advisers translating institutional credit frameworks for private clients. It assumes financial literacy but not prior private-credit experience.

How this applies to live mandates

Matchpoint Partners arranges private-credit transactions across the GCC, India and the UK — and places credit funds and co-investments with family-office capital. The framework in this paper reflects how we help allocators interrogate the opportunities we and others bring them: purpose first, structure second, yield last. Talk to a partner about building or stress-testing your allocation.

Building a Private Credit Allocation — frequently asked questions

There is no universal number — it depends on the portfolio’s income needs, liquidity profile and existing equity risk. The paper’s framework starts from the role the allocation must play and derives sizing from that, alongside pacing rules that build exposure across vintages rather than in a single deployment.

Both outcomes are available. Senior, covenant-protected lending to sound borrowers behaves very differently from aggressively structured junior credit, even when quoted yields look similar. The paper explains how to read structure, seniority, documentation and manager incentives so the allocation delivers the risk profile it promises.

The spectrum runs from senior direct lending — secured, covenant-protected loans at the conservative end — through mezzanine and special situations to asset-backed and speciality finance. Risk, yield and liquidity trade off along that spectrum: senior strategies prioritise capital protection and steady income, while junior and opportunistic strategies reach for return by accepting structural subordination or complexity.

It depends on internal capability. Commingled funds suit allocators who want diversification with minimal infrastructure; separately managed accounts offer control and fee advantages for larger commitments; direct lending demands genuine origination and workout capability that few family offices possess at the outset. Most programmes begin with funds and add directness as capability matures.

Across more dimensions than most first-time allocators expect: managers, strategies, vintages, sectors and geographies. Concentration in a single manager or deployment year is the trap that catches allocators chasing headline yield. Building exposure steadily across vintages also means the book seasons gradually, so performance problems surface while the programme can still adapt.

Want to act on this research?

Talk to a partner about how it applies to your transaction.