The J-Curve Problem: Managing Liquidity and Pacing in a Family Office Private Markets Programme

Managing liquidity and pacing through the J-curve in a family-office private-markets programme.

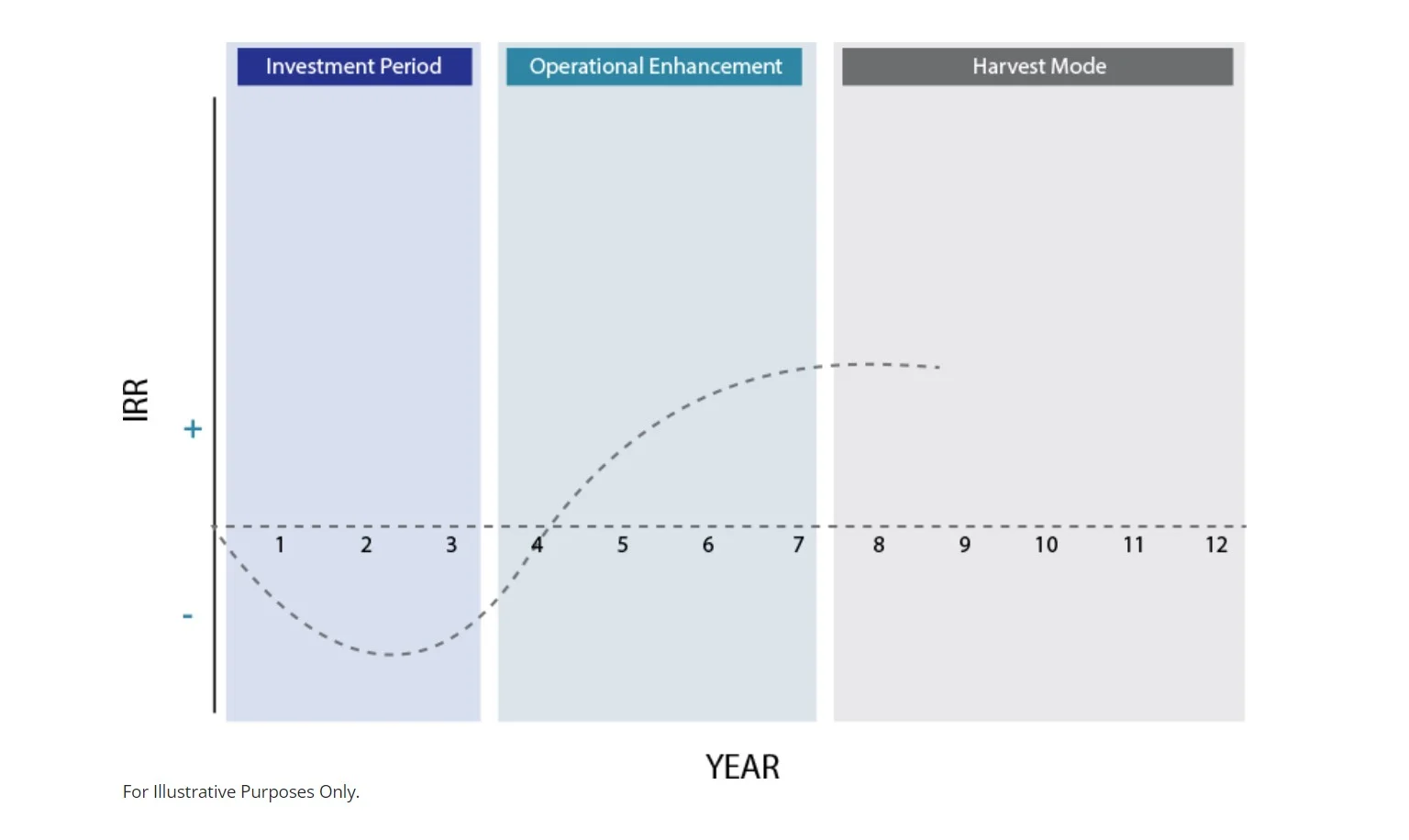

Early in a private markets programme, capital calls and fees run ahead of distributions, pushing cumulative cash flow negative before it recovers. This paper sets out a pacing and liquidity framework that helps family offices commit steadily across vintages, size reserves sensibly and bridge the J-curve without holding excessive idle cash.

Managing liquidity and pacing through the J-curve in a family-office private-markets programme.

Part of Matchpoint Partners' proprietary research programme — original, data-driven analysis grounded in live deal experience. Read the full paper: framework, structures, worked examples and data.

Read the full research paper Explore our Alternatives practice

What this paper examines

The paper addresses the defining cash-flow problem of any new private markets programme: the J-curve. In the early years, funds draw capital and charge fees while their investments are still maturing, so the programme consumes cash long before it returns any. A family office that has not planned for this pattern faces an uncomfortable choice — hold large idle reserves that drag on returns, or run thin and risk being unable to meet a capital call.

The author develops a commitment-pacing framework that smooths this curve by spreading commitments across vintage years, sizing liquidity buffers against stressed scenarios rather than averages, and using bridging tools such as NAV-based facilities and secondary purchases where appropriate. The analysis also covers allocation drift and the denominator effect — the complications that arise when public portfolio values move while private valuations lag — with particular attention to the circumstances of GCC family offices.

Why it matters now

Gulf family offices are shifting meaningful capital from public markets into private alternatives, and many are building their first structured programme rather than making one-off fund commitments. The J-curve is most punishing for first-time programmes, where every vintage is young at once and there are no older funds distributing cash to fund the new ones. Getting pacing and reserve policy right at the outset is far cheaper than correcting a liquidity squeeze — or a forced secondary sale — later.

Key questions it answers

- Why do private markets programmes turn cash-flow negative in their early years, and for how long should an allocator plan to fund that deficit?

- How should commitments be paced across vintages so that later distributions begin to fund earlier calls?

- What liquidity reserves are appropriate, and how should they be stress-tested rather than sized on average conditions?

- When do NAV facilities, secondaries and other bridging tools genuinely help — and when do they simply add leverage to a liquidity problem?

Who should read it

Principals, chief investment officers and investment committee members of single and multi-family offices that are building or scaling a private markets programme, together with treasurers and finance heads responsible for meeting capital calls. It will also interest wealth advisers who help families translate a target allocation into an actual commitment schedule.

How this applies to live mandates

Matchpoint Partners advises family offices on precisely these decisions: structuring commitment programmes, sourcing secondary opportunities that shorten the J-curve, and arranging NAV-based and other portfolio-level financing where bridging liquidity is needed. The framework in this paper reflects the questions we work through with clients on live mandates — read the full paper for the models, worked examples and data behind it.

The J-Curve Problem — frequently asked questions

The J-curve describes the typical shape of cumulative cash flows in a private markets programme: negative in the early years, recovering later. It happens because funds draw capital and charge fees while investments are still maturing, so cash goes out long before distributions return. The full paper sets out how to plan for it.

The core tools are commitment pacing across vintage years, holding a liquidity reserve sized against stressed scenarios, and using bridging mechanisms such as secondary purchases or NAV-based facilities where appropriate. The paper provides a framework for combining these so the programme grows steadily without either idle cash drag or funding shortfalls.

It is the discipline of spreading fund commitments steadily across vintage years rather than deploying in one or two. Pacing smooths the J-curve — later distributions begin to fund earlier capital calls — diversifies the programme across market conditions, and prevents the whole portfolio being young, cash-hungry and exposed to a single vintage at once.

Against stressed scenarios rather than averages. Capital calls cluster and distributions dry up at precisely the same moments — typically in market downturns — so a reserve sized on normal conditions fails exactly when it is needed. The framework balances that protection against the opposite error: holding so much idle cash that it drags on overall returns.

Yes — purchasing existing fund interests means acquiring positions that are already partly invested and closer to distributing, so the programme reaches positive cash flow sooner than with primary commitments alone. Secondaries are one of the principal bridging tools the paper examines, alongside NAV-based facilities, with the usual caveats on pricing, selection and diligence.

Want to act on this research?

Talk to a partner about how it applies to your transaction.