The Mezzanine Gap: Filling the Space Between Senior Debt and Equity in GCC Real Assets

Filling the mezzanine gap between senior debt and equity in GCC real assets.

Between the senior debt a lender will provide and the equity a sponsor can raise lies a gap — too risky for senior debt, too valuable to fund with expensive common equity. Mezzanine capital fills it, increasing leverage and reducing the equity cheque without diluting ownership. This paper explains how it works in GCC real assets and when it makes sense.

Filling the mezzanine gap between senior debt and equity in GCC real assets.

Part of Matchpoint Partners' proprietary research programme — original, data-driven analysis grounded in live deal experience. Read the full paper: framework, structures, worked examples and data.

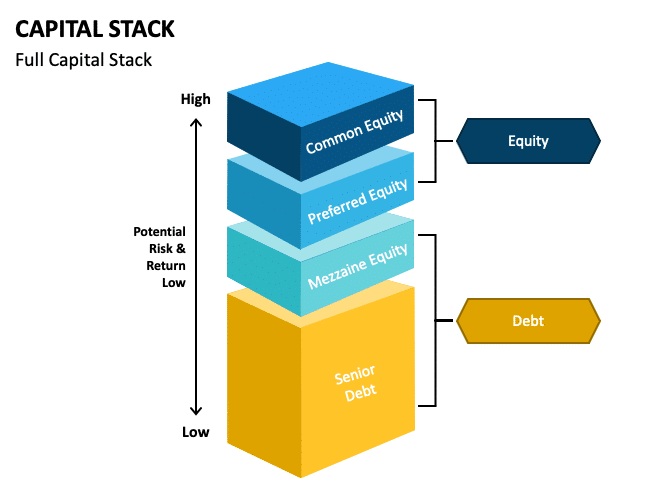

What this paper examines

The paper examines the layer of the capital structure that sits between senior debt and common equity in GCC real-asset transactions. Senior lenders stop at a level of leverage set by their risk appetite; the remainder has traditionally been funded with equity — the most expensive capital a sponsor has. Mezzanine capital, in the form of subordinated debt or hybrid instruments, occupies the space between.

It sets out the forms mezzanine takes — subordinated loans, preferred equity and hybrid structures — how each ranks and is secured, what mezzanine does to overall leverage and to equity returns, and the structuring considerations that determine whether a given transaction can support it. Intercreditor dynamics between senior and mezzanine lenders receive particular attention.

Why it matters now

Gulf real-asset sponsors have historically faced a binary market: conservative senior debt or full equity. As regional private credit deepens, a genuine mezzanine layer is emerging — and with it the ability to complete capital stacks that previously stalled, hold assets through transitions, and stretch equity across more projects. Sponsors who understand how to use the instrument — and when not to — gain a meaningful structural advantage over those still operating in the binary world.

Key questions it answers

- What forms does mezzanine capital take, and how do subordinated debt, preferred equity and hybrids differ in practice?

- How does adding a mezzanine layer change leverage, the equity requirement and the sponsor’s returns?

- What do mezzanine providers require — security, intercreditor terms, exit visibility — before committing?

- How should a sponsor decide whether a transaction genuinely supports mezzanine, or whether the gap is better closed another way?

Who should read it

Developers and sponsors whose projects stall between what senior lenders will provide and the equity they wish to commit; family offices evaluating mezzanine as an investment offering equity-like returns with debt-like protections; and senior lenders who want to understand the layer forming beneath them in the capital stack.

How this applies to live mandates

Arranging mezzanine and development-gap funding is a named practice area at Matchpoint Partners, and the structuring considerations in this paper — ranking, intercreditor terms, return composition — mirror the negotiations we run on live capital-stack mandates across the Gulf. The full paper develops the analysis with case studies and sensitivity work; readers should consult it for the supporting data.

The Mezzanine Gap — frequently asked questions

Mezzanine is capital that ranks between senior debt and equity — typically subordinated loans, preferred equity or hybrid instruments. It lets a sponsor raise more of the capital stack as debt-like funding, reducing the equity cheque without giving up common ownership, in exchange for a higher cost than senior debt.

Broadly, when the gap between available senior debt and the sponsor’s equity is real, the project’s returns can absorb the higher cost, and there is a credible exit — sales, refinancing or stabilisation — within the facility’s term. The paper provides a framework for testing each condition.

Mezzanine debt is a subordinated loan — contractual interest, a maturity date and typically some security — while preferred equity is an ownership instrument carrying a priority return but no creditor claim. They occupy the same layer of the capital stack and serve similar purposes; the choice affects security, intercreditor treatment and flexibility.

Because the intercreditor agreement governs the relationship between senior and mezzanine lenders — payment priorities, enforcement rights, standstill periods and cure rights. Those terms determine what the mezzanine provider can actually do if the project comes under stress, and senior lender requirements often shape whether a mezzanine layer is feasible at all.

By replacing part of the equity cheque with capital that costs less than equity’s expected return, mezzanine can lift returns on the equity the sponsor does commit — and stretch that equity across more projects. The effect cuts both ways: higher leverage amplifies the downside too, so project returns must genuinely absorb the cost.

Want to act on this research?

Talk to a partner about how it applies to your transaction.